It’s been said that more money has been lost due to indecision than was ever lost because of a bad decision. Regardless of whether you agree with the statement, delaying the decision to buy in today’s market is going to cost the buyer more.

It’s been said that more money has been lost due to indecision than was ever lost because of a bad decision. Regardless of whether you agree with the statement, delaying the decision to buy in today’s market is going to cost the buyer more.

Home prices have gone up considerably in almost every market in the country in the past year and while inventories are beginning to grow, prices are expected to continue to rise. Mortgage rates jumped 1% from the beginning of May to now. They could easily reach 5% by the end of the year and continue to rise in 2014.

Many of the financial experts in the country believe that the economy will not be strong until rates are in the 7% area.

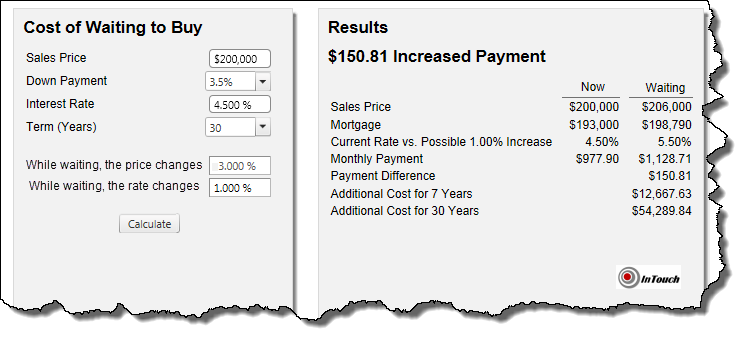

The two components that move the cost of housing are price and mortgage rates. Escalation of either one will have an affect but when both are going up simultaneously, it is dramatic. It can literally eliminate buyers who could have purchased earlier.

The following example shows what would happen to the payments on a $200,000 home if the price were to go up 3% at the same time that the mortgage rates went up 1%. Not only would the payments go up by $150.81 per month, the price of the home would be $6,000 more. Even though the down payment may not change much, the new owner would have to borrow more money. By not acting, it is costing them more in price and payment. The loss of the appreciation would have been equity had they purchased prior to the rise in price.

You’ve saved for a rainy day or retirement. Congratulations but don’t get too comfortable yet; where is it invested? It’s estimated that over 25% of Americans have their long-term savings in cash instead of investments like stocks, bonds or real estate.

You’ve saved for a rainy day or retirement. Congratulations but don’t get too comfortable yet; where is it invested? It’s estimated that over 25% of Americans have their long-term savings in cash instead of investments like stocks, bonds or real estate.

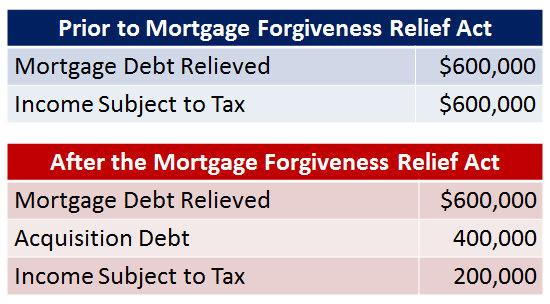

Many times a homeowner might feel relieved being out from under the obligation of a mortgage they can’t afford even though the property was lost due to foreclosure or short sale. If a lender cancels or forgives debt, a taxpayer must include the cancelled amount in their income for tax purposes depending on the circumstances. The tax significance could be serious.

Many times a homeowner might feel relieved being out from under the obligation of a mortgage they can’t afford even though the property was lost due to foreclosure or short sale. If a lender cancels or forgives debt, a taxpayer must include the cancelled amount in their income for tax purposes depending on the circumstances. The tax significance could be serious.

Inventory is dramatically shrinking and it is commonplace in many markets to have multiple offers on a home. While the sellers would prefer to be able to choose the best offer for them, it can be incredibly frustrating for the buyers who might consider the following tips to get their offer accepted.

Inventory is dramatically shrinking and it is commonplace in many markets to have multiple offers on a home. While the sellers would prefer to be able to choose the best offer for them, it can be incredibly frustrating for the buyers who might consider the following tips to get their offer accepted.