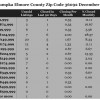

These were the existing Homes for Sale December 2013 for Zip Code 36092 in Wetumpka, Holtville, Dozier, Wallsboro, Lake Jordan and Elmore County including subdivisions Cotton Lakes, Jordan Trace, River Oaks, Macon Place, Cherokee Estates, Stone River, Country Club Estates, Cadens Creek, and Foxfire. How to use: Find the Price Range in which your home falls. This will show the number of active listings (your competition if you are selling your home), the number of homes that closed in the last 90 days, the number of homes that close on average in a month, the Percentage Closed Monthly (the likelihood that one home will close in a month), and the Months of Inventory (how many months worth of homes to sell if no other homes come on the market). A high Months of Inventory figure indicates a better chance of a bargain if you are buying. For a personalized report, feel free to contact me.

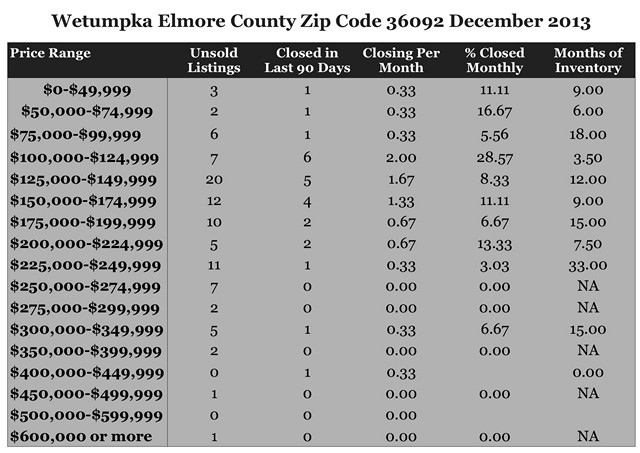

December 2013 Home Sales Zip Code 36092

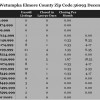

December 2013 Home Sales Zip Code 36093

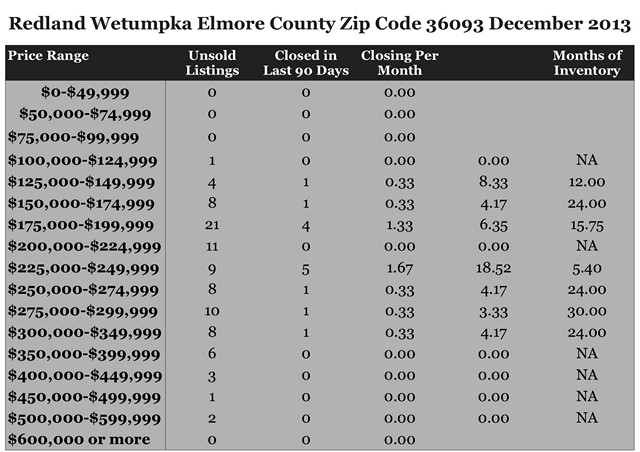

These were the existing Homes for Sale in December 2013 for Zip Code 36093 in Redland, Wetumpka, and Elmore County including the subdivisions Emerald Mountain, Blue Ridge, Mitchell Creek Estates, Grand Ridge, Jasmine Hill, Stonegate, Windsong Ridge, Wildwood, Harrogate Springs, Jackson Trace, and Brookwood. How to use: Find the Price Range in which your home falls. This will show the number of active listings (if you are selling this is your competition), the number of homes that closed in the last 90 days, the number of homes that close on average in a month, the Percentage Closed Monthly (the likelihood that one home will close in a month), and the Months of Inventory (how many months worth of homes to sell if no other homes come on the market). A high Months of Inventory figure would indicate a chance of a better bargain for a buyer. For a personalized report, feel free to contact me.

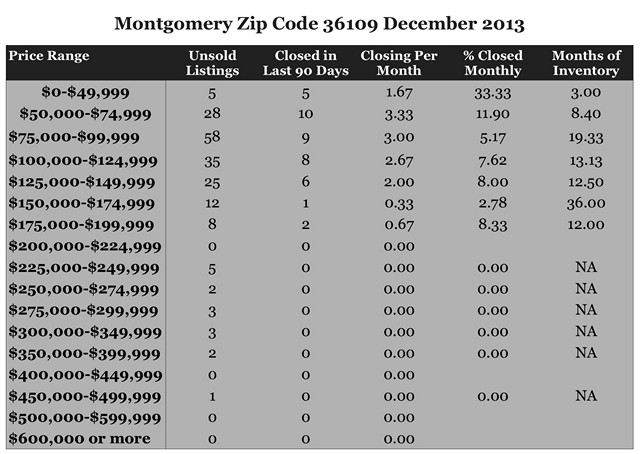

December 2013 Home Sales Zip Code 36109

These were the existing Homes for Sale December 2013 for Zip Code 36109 in Montgomery including subdivisions Forest Hills, Lakeview Heights, Dalraida, Johnstown, Morningview, Bell Hurst, County Downs,Fox Hollow, and Carol Villa. How to use: Find the Price Range in which your home falls. This will show the number of active listings (your competition if you are selling), the number of homes that closed in the last 90 days, the number of homes that close on average in a month, the Percentage Closed Monthly (the likelihood that one home will close in a month), and the Months of Inventory (how many months worth of homes to sell if no other homes come on the market). A high Months of Inventory figure indicates a better chance for a bargain if you are buying. For a personalized report, feel free to contact me.

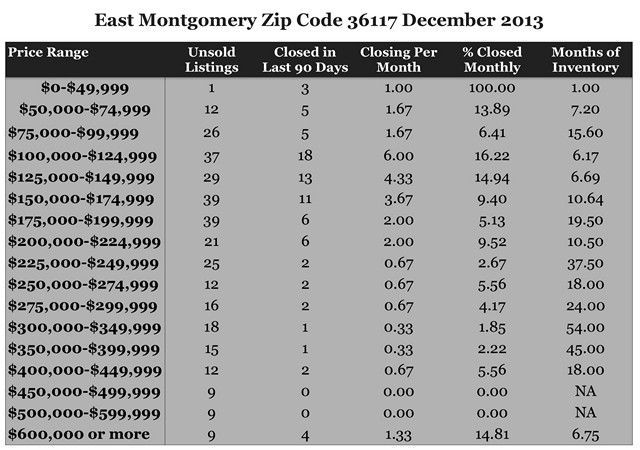

December 2013 Home Sales Zip Code 36117

These were the existing Homes for Sale December 2013 for Zip Code 36117 in Montgomery including subdivisions Montgomery East, Halcyon, Halcyon Summit, Copperfield, Dexter Ridge, Woodmere, Bellwood, Thorington Trace, Deer Creek, Lake Forest, Arrowhead, Towne Lake, Somerset, Wynridge,and Wynlakes. How to use: Find the Price Range in which your home falls. This will show the number of active listings (your competition if you are selling), the number of homes that closed in the last 90 days, the number of homes that close on average in a month, the Percentage Closed Monthly (the likelihood that one home will close in a month), and the Months of Inventory (how many months worth of homes to sell if no other homes come on the market). A high Months of Inventory figure indicates a better chance for a bargain if you are buying. For a personalized report, feel free to contact me.

Up to $500 for Doing Home “Work”

The energy-efficient home upgrades tax credit is scheduled to expire on December 31st this year. If you need to make improvements to your home, this could be an incentive to do it before the end of the year. If you have already made qualifying improvements without realizing the tax credit is available, it may seem like a holiday gift you weren’t expecting.

The equipment must be installed to qualify for the credit which can put you under a time crunch. Heating and cooling systems, insulation, windows, doors, skylights, water heaters and home weatherization may qualify.

The Residential Energy Efficiency Tax Credit has been available for purchases since January 1, 2011. The tax credit is 10% of up to $5,000 of qualifying improvements which would make a maximum of $500 tax credit.

The cumulative maximum amount of tax credit that can be claimed by a taxpayer in the different years this law has been in effect is $500. If it has been claimed in previous years, the taxpayer is not eligible for this credit for additional new purchases.

For more information, see energy.gov or talk to your tax professional.

Winter Maintenance

With a 2,000+ mile long winter storm affecting much of the country, there are plenty of home owners who wish they were better prepared. Even when you live in warm climates, some of these things are important to check periodically.

Preparing for the change of seasons can make your home more comfortable and protect your investment. Regular maintenance extends the various components of a home and can generate savings in operating costs while avoiding expensive replacements.

- Weather strips around doors and windows should be checked for possible air leaks.

- Caulking around windows and doors should seal out moisture and air leaks.

- HVAC should be inspected and serviced by a professional annually.

- Smoke and carbon monoxide detectors should be tested regularly.

- Ductwork and supply lines from water heaters should be insulated.

- Fireplace chimneys should be cleaned regularly and fireplaces should be inspected for cracks in mortar and to see if the damper closes properly.

- Gutters should be free of leaves and debris to prevent rainwater build-up.

- Tree branches touching or hanging over your roof should be trimmed.

Please contact us if you need a service provider recommendation.

Motivated Sellers, Better Prices and Less Competition

The Winter Home Buyer Report conducted in the second week of November by REALTOR.com® revealed the sentiments of current home buyers expecting to buy a house during the winter months. It appears that there is pent-up demand with buyers who were unable to purchase a home recently.

Most cited as an impediment to purchase was the challenge of low inventory. Strong demand coupled with short supply explains why home prices have been increasing.

“This summer and spring home buying season was particularly challenging for buyers, especially first-time home buyers trying to compete with all-cash offers and bidding wars because of reduced inventory. In fact, a quarter of the winter home buyers revealed they are in the market now because they were unable to find a home during this last home buying season,” said Alison Schwartz, vice president of corporate communications at REALTOR.com®. “While buyers are still experiencing challenges with inventory and approximately one in five buyers plan to put down all cash, there are advantages to looking for a home in the winter. Motivated sellers, better prices and less competition between buyers are some of the top reasons winter home buyers are interested in purchasing a home during the colder months of the year.”

Some interesting statistics taken from the report are:

Biggest challenges when searching for a home during winter:

• 34 percent shared that there is not enough inventory on the market

• 29 percent believe that winter weather makes house hunting unpleasant

Traditionally, the industry has found that the fourth quarter of the year has a lower sales volume and is generally attributed to distractions from the holidays and not wanting to make a move during consistently inclement weather. Even in areas that are not affected by extreme winter weather, there seems to be a mindset about moving in the winter.

Indications are that it may be advantageous for sellers to put their home on the market now rather than wait until after the first of the year.

Refinance to Remove a Person

Most people are familiar with the various reasons a homeowner refinances their home which generally result in two major benefits: saving interest and building equity.

There is however another reason to refinance which may not be as common which is to remove a person from the loan. In the case of a divorce, when one party wants to keep the home and the other party wants their equity out of the home, it is possible for the remaining party to refinance the home. If the equity is sufficient to justify it and the remaining owner can qualify for the new loan, the refinance can provide the proceeds to buy out the other spouse.

Refinancing to remove a person from the loan could also involve a situation where two or more heirs jointly own a property and have differing opinions on when to sell. The same situation could apply to a rental property with multiple owners and the refinance would provide a way to buy out a partner.

Sometimes, it’s not about taking cash out of the home to buy out the other party. If a person’s name is on the mortgage, they’re responsible if it goes to default. One party may be willing to deed the home to the other party but it doesn’t necessarily relieve them of the liability of the mortgage they originated.

Many times, once a person has made their mind to move on, they’ll take the fastest and easiest way out. Removing a person from the deed or a mortgage is a reason to consider obtaining legal advice to protect your interests. Refinance Analysis calculator.

Reasons to Refinance

1. Lower the rate

2. Shorten the term

3. Take cash out of the equity

4. Combine loans

5. Remove a person from a loan

Who’s Paying Your Mortgage?

As a homeowner, you obviously pay for your mortgage but as an investor, your tenant does. Equity build-up is a significant benefit of mortgaged rental property. As the investor collects rent and pays expenses, the principal amount of the loan is reduced which increases the equity in the property. Over time, the tenant pays for the property to the benefit of the investor.

Equity build-up occurs with normal amortization as the loan is paid down. It can be accelerated by making additional contributions to the principal each month along with the normal payment. Some investors consider this a good use of the cash flows because interest rates on savings accounts and certificates of deposits are much lower than their mortgage rate.

In the example below, is a hypothetical rental with a purchase price of $125,000 with 80% loan-to-value mortgage at 4.5% for 30 years compared to a 3.5% for 15 years. The acquisition costs were estimated at $3,000, the monthly rent is estimated at $1,250 and $4,800 for operating expenses.

Notice that both properties have a positive cash flow before tax. The cash on cash return is the revenue less expenses including debt service divided by the initial investment to acquire the property. The 15 year mortgage will obviously have a smaller cash flow and lower cash on cash but the equity build-up is significantly higher.

If the goal of the investor is to pay off the property to provide the highest possible cash flow at a later date, a shorter term mortgage with a lower interest rate will help them achieve that. A simple definition of an investment is to put away today so you’ll have more tomorrow. Sacrificing cash flow now, during an investor’s earning years, is a reasonable expectation to provide more cash flow in the future when it might be needed more.

Contact me if you’d like to explore rental property opportunities.

All Dollars Not Equal

The division of assets between the spouses is an important decision to finalize a divorce. The exercise looks relatively simple: assign a value for each of the assets and divide them based on a mutual agreement between the parties.

The challenge is to make a fair division which requires an analysis to determine their value after they’re converted to cash.

Assume the two major assets in the example, a retirement account and the equity in the home, are equal at $100,000. It might seem logical to give the home to one spouse and the retirement account to the other. However, if the person receiving the home decides to sell the home, the net proceeds could be considerably less than the spouse receiving the retirement account.

Let’s pretend that the spouse with the home negotiates a lower price of $475,000 due to current market conditions. The former couple had owned the home for many years and refinanced several times, pulling money out of the home each time. When the remaining spouse sells the home, there could be a considerable gain that was never recognized.

As a single person, he or she is now only entitled to $250,000 exclusion and would have to pay tax on the excess gain. After paying the sales costs, outstanding mortgage balance and the taxes due on the gain, the remaining spouse would have net proceeds of $24,375 compared to the $100,000 that the former spouse received in the settlement.

The message in an example like this is to examine and consider the potential expenses that may be involved with converting the assets to cash after the divorce. Obviously, expert tax advice is valuable in making such decisions.